If you follow us regularly, you know: we are investing globally in construction technology and building materials technology. Part of the reason why we choose to be global, cross-border VC investors is that it puts us in the position to identify patterns and indicators for emerging investment trends across the markets. Tiger Global has proven for many years how a truly global VC can achieve outsized returns.

The basic premise of our approach to identifying the big innovation opportunities in construction is that markets are complex adaptive systems. This means that the behaviors of customers and competitors are adapting to each other and to how the market evolves over time. The long-term outcomes of innovations are a result of how those emergent behaviors unfold in the market. We loosely define long-term as “more than 5 years out”. This long-term result is hard to perfectly predict early on because you have to get multiple assumptions right at the same time. Our friends over at Benchmark made this dogma famous:

“Throw that crystal ball out, you can’t perfectly predict anything. What you can do is discover when lightning strikes.”

— Peter Fenton, Benchmark

What we observed additionally is that timing plays a major role in picking rising tides and innovation opportunities. Big opportunities tend to emerge at the intersection of need<>technology<>timing. Timing is the often underrated factor. Consider these two examples:

In early-stage investing, timing is the hardest to observe. That also means: if we observe a ride rising in multiple construction markets at around the same time — or a few months after each other — we are significantly more likely to catch opportunities with outsized return potential.

What we have learnt is that timing can only be observed by being in close touch with the customers, entrepreneurs and experts in construction. We cannot observe from the desk when lightning strikes. We extensively use our network of construction experts and operators to validate whether venture opportunities we see in construction match with timing in the market — so far (as per March 2020) into more than 7’000 ventures in the construction sector across Asia, Australia, North America, Europe and Africa.

(Update December 2020: now at 12’000 and counting…)

Based on this data set, we recently refined our 10 principles how we go at discovering the rising tides in construction markets across the globe:

Markets are complex adaptive systems. For that reason it is impossible to predict with certainty the outcomes of any opportunity we see. Which of these opportunities will succeed and pay off will become apparent only during or after the fact, because their success will emerge from how the complex markets adapt to the innovations. Ergo: it is possible to discover success over time from within a portfolio of 30+ opportunities that create optionality. This is what innovation investors fundamentally do — they do not try to perfectly predict the outcome of any single opportunity, but they build a portfolio so they can discover which ones are becoming successful, and then double down on the winners.

Because markets are complex adaptive systems, our job is not to predict the future. Our job is to see the present very clearly. Our job is to observe the patterns that are unfolding in front of us. Our job is not to augur — our job is to observe when lightning strikes, and move decisively to benefit from it.

Gall’s law states: “A complex system that works is invariably found to have evolved from a simple system that worked. A complex system designed from scratch never works and cannot be patched up to make it work. You have to start over with a working simple system.” Any ultimately huge opportunity in the construction sector will look tactile and simple right now. For this reason, we are absolutely obsessed with founders who tell us a big tactile change they want to effect in construction — not an abstract or fringe idea.

Without a moat, competition will ultimately inevitably drop prices and compress margins to a point where there is no economic profit and the investments we made are burnt. In opportunities that appear certain because there are no emerging behaviors, competition will likely already be entrenched. No amount of defensibility can typically create outsized investment returns for us. We always opt to stay out of opportunity where there are no emerging behaviors. Instead, we look for spaces where we discover differentiating emerging tech, customers beginning to spread the word, and unique partnerships and business models emerging. And then we back the team that has what it takes to become the defensible #1 or #2 player in their space.

“What’s the number one form of differentiation in any industry? Being number one.”

— Marc Andreessen, Andreessen Horowitz

In picking growth opportunities we will face a business strategy trade-off: do we prefer opportunities with initially high margins over opportunities with initially low margins. Picking opportunities with currently high margins looks enticing. But: generally, higher margin opportunities in B2B tend to grow more slowly due to slower sales cycles and slower cash flow. This creates slower discovery and low optionality. Instead, it can be smarter to think about opportunities in ways how we can make them ultimately (not necessarily initially) defensible in order to increase margins at that point in time and how we can blitzscale them. Counter-intuitively, intentionally accepting low margins to increase fast adoption, growth and discovery can be the lower risk and higher return approach.

Technology outcomes are more linearly predictable than market outcomes. Ergo: we are more inclined to exploit big opportunities where we begin to observe emerging market demand and where technology can provide us defensible advantages, than accepting opportunities where market demand is entirely unclear and where technological differentiation is hard to achieve.

Because markets are complex adaptive systems, there are probably three to four things out of ten we can control that matter for the success of our growth opportunities (we stole this with pride from our friends over at Khosla — couldn’t have said it any better). Our competitors will control another three or four. The rest are unknown to us before the fact (i.e. luck, believe it or not). For this reason, we must consider that our opportunities must be driven by people who excel at adapting in fast-paced adaptive environments and who have an outsized will to succeed. Only such people will allow us to grow and discover fast, and create optionality for us over time. The single most certain choice we can make before the fact is picking A+ people.

Returns of innovation opportunities strongly tend to distribute along a power law distribution (aka fat tail). This means that a handful of opportunities in the construction sector will generate outsized returns in excess of 40x on investment. 50% of all opportunities will usually be total write-offs. The remaining opportunities will generate low return multiples.

Power law distributions are the other key reason why a portfolio of growth investments is so important to discover and double down on the winners as they unfold over time. This is the single most important concept of investing in emerging growth opportunities. Any single opportunity without discovery and optionality is more likely to be on the low-return end of the power law distribution. Fast discovery + optionality + doubling-down on the winners.

Because innovation opportunities distribute along power law, and because markets are complex adaptive systems, the opportunities we go after must have the chance to be worth our while. In other words: each single growth opportunity we pick as part of our portfolio must be big and bold enough to generate outsized returns.

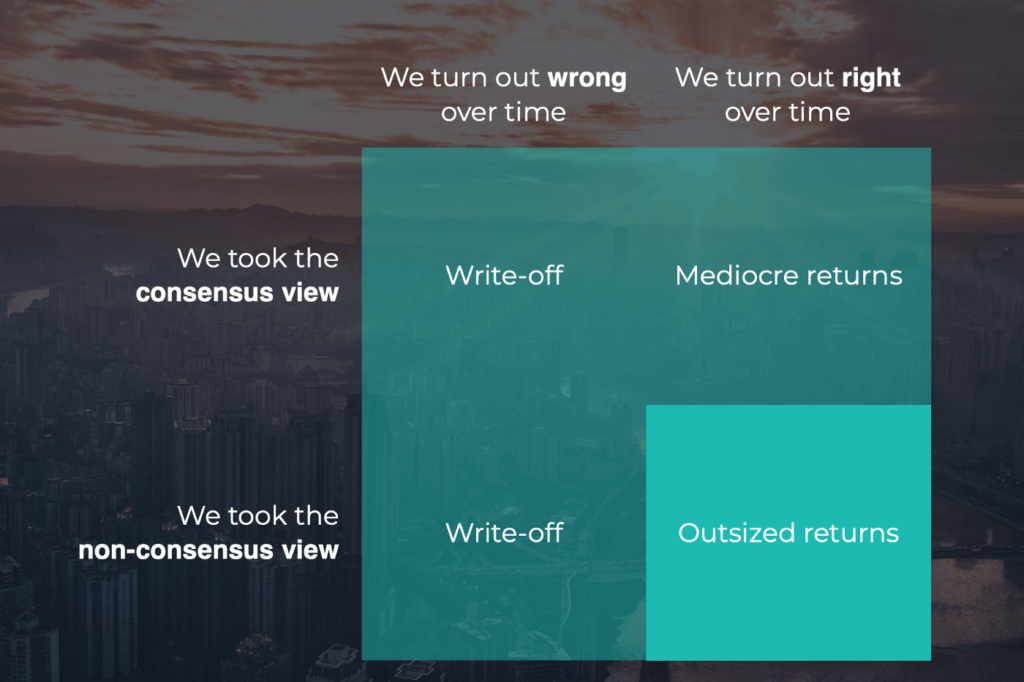

The problem is: we cannot outperform markets by starting with consensus views due to competition and information symmetry.

Ergo: we must focus on growth opportunities in which non-consensus edge views can allow us to outperform in the construction markets. Only over time we will discover which opportunities actually do generate power law returns. However, if we start with consensus views, none of those opportunities will generate power law returns for us and most likely we will not return our investments as a whole.

Zeckhauser’s Law states that when others know the likely outcomes of an opportunity better than us, chances are that those others will use this information asymmetry to our disadvantage. Ergo: we stay away from opportunities in which there are already people who can predict the outcome with high certainty when we can’t. Ergo: we only go after opportunities in which everybody (incl. ourselves) either does or does not know the likely outcome yet.

Let’s use the example of a B round to bring home our points. Imagine two companies we could invest in — and we are not yet existing investors.

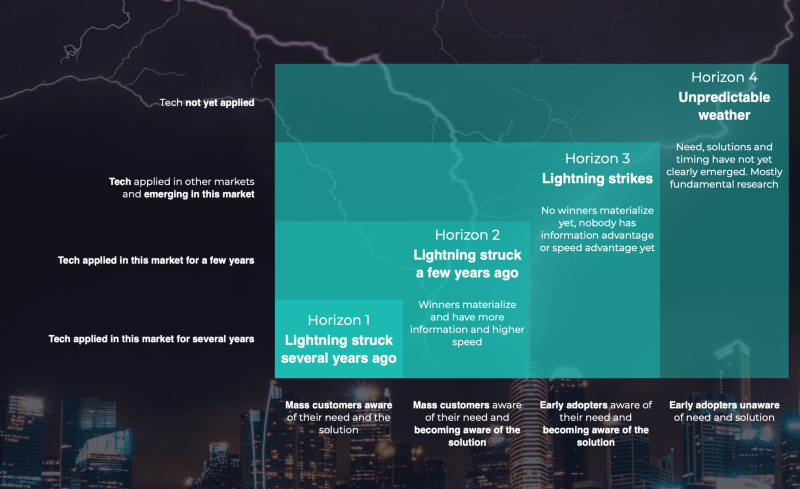

Company 1 is in a space in which our observations tell us that winners will materialize in the near future — mass customers are aware of their need, and become aware of the various solutions. The tech has been applied for a few years. Now company 1 raises their B round to grow domestically, and existing investors would allow us to lead or co-lead their round. The problem is: as the space is nearing mass market, we are very likely at an information disadvantage over existing investors. Zeckhauser teaches us: if existing investors let us lead a such a round, we should assume that it is very likely that Company 1 is not going to be #1 or #2 in their market. Entering opportunities when they are in Horizon 2 is a losing territory.

Company 2 is raising their B round in a space that is a bit younger. The tech has been applied in other markets before (!), but in this market only for 2–3 years really (the company was fast). They commercialized so far on a few early adopting enterprise clients, and landed and expanded within these enterprise accounts. The question still is: when are mass customers going to begin adoption. Some kinks on the tech and product remain. 3 to 4 competitors exist. When we see a space like this, we can reasonably assume that inside investors are not entirely certain of the winner as well. What we try to do in such an opportunity is to identify patterns and winners from other global markets in the same space — and transfer those patterns to make a judgment on the likely further trajectory of Company 2. This gives us an information advantage. We love entering companies at such stages !

We call this stage Horizon 3. Horizon 3 is where lightning strikes right now at the intersection of need<>technology<>timing.

The above B round just serves as an example. We invest with our currently two funds from seed/pre-revenue through Series B, all the way. A Horizon 3 opportunity can exist at any company stage.

If you feel you are building the next big power law opportunity in ConstructionTech in a horizon 3 space — come talk to us !