We were asked many times since we started Foundamental 2.5 years ago:

What is the difference between ConstructionTech and PropTech?

What sounds like a straightforward question has brought even veteran industry insiders to the verge of despair and hair-loss. Interestingly, by far the largest group of folks asking us are asset owners and investors. By my – totally scientific un-scientific – estimate, 90%+ of folks asking us are large institutional investors and real estate investors. It points to an increasing interest into ConstructionTech we have been observing lately.

On the other hand, we spoke to thousands of founders in 2020, and most of them quite clearly expressed the distinctive differences. Many of these founders don’t even come from a real estate or construction background – and yet seem to have a clear view of the differences.

However, founders told us they get the same question from their investors, who can be generalist venture capital firms looking at many different sectors.

So, we thought, let’s share the distinctive features how we see them – and put this question to bed once and for all.

Let’s kick it off with textbook definitions. According to the Cambridge Dictionary:

“Property Management is the management of land and buildings as a business, including keeping buildings in good condition and renting property”

while

“Construction is the work of building or making [or renovating] something, especially buildings, bridges, etc.”

In other words, construction is about creating and selling assets from scratch, while property management is about utilizing and re-selling existing assets.

Makes abstract sense, so far. Still, doesn’t help much when you’re an investor or a founder. Let’s try another way.

Both sectors have in common that they transact big immobile assets. That means, both require mastery of the financial side, especially topics such as creating liquidity through loans, escrows, working capital management and insuring risks.

The differences lie elsewhere.

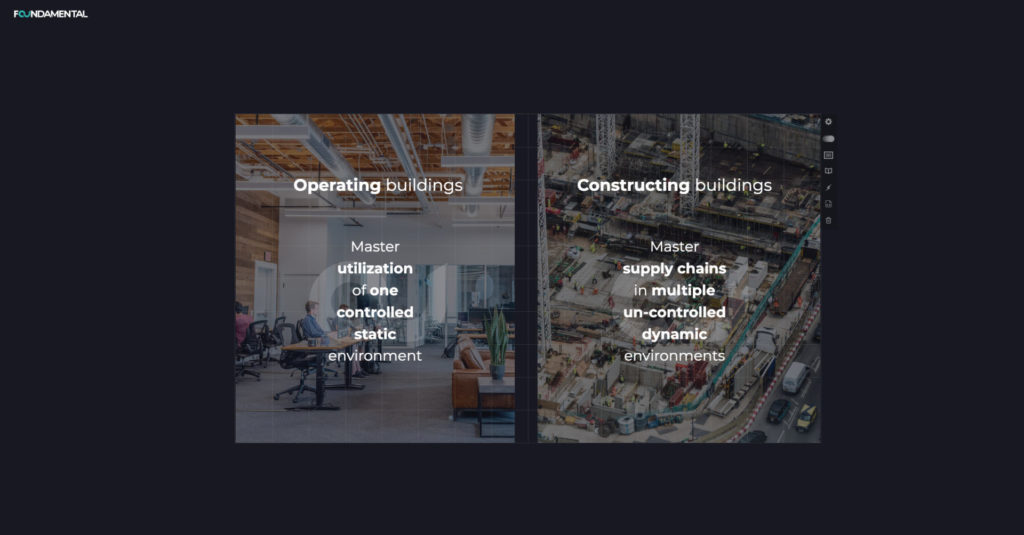

To master ConTech, you have to master supply chains. To master PropTech, you have to master utilization.

ConTech deals with multiple uncontrolled and dynamic environments, while PropTech almost always deals with one controlled and static environment. That’s because PropTech addresses assets that already exist, and as such, knows the parameters of the asset and its surroundings. Property management supply chains are often simpler and linear.

On the other hand, construction supply chains have to account for a wide range of factors not in control of the owner, eg. weather, traffic and workforce, as well as inter-dependencies (if my plumbing materials don’t arrive on time I must reschedule my tile works).

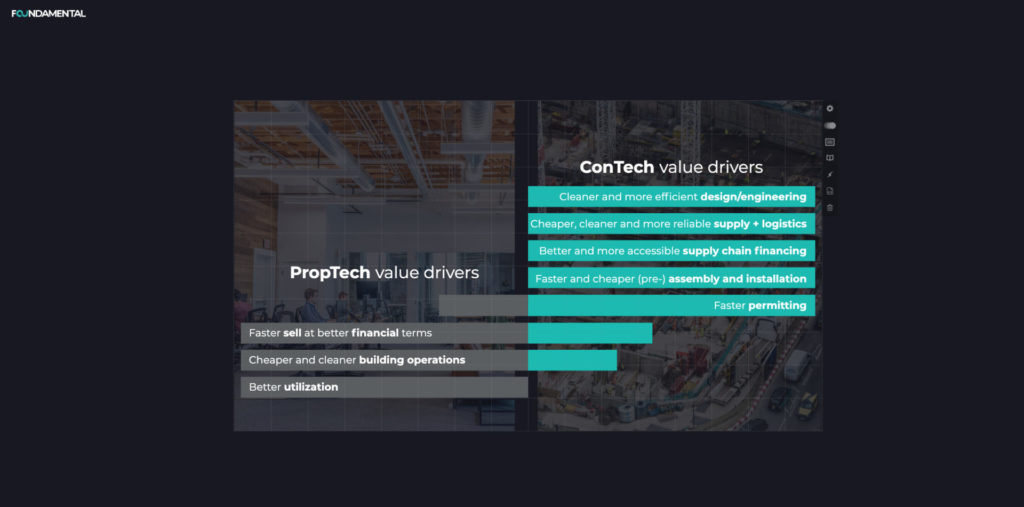

Without claiming to be exhaustive: In PropTech, technology helps to increase asset utilization, decrease building operations cost and re-sell an asset at better financial terms.

We see most PropTech address the same four levers:

In ConTech, the value of technology plays out differently. Tech serves to create control over supply chains and fulfillment. This begins how we engineer and design the asset and which materials we use, as these decisions can have major impact at how supply and logistics can be optimized. That’s why ConTech attacks a wide range of levers to create value:

To master ConTech, you have to master supply chains. To master PropTech, you have to master utilization.

Let’s also talk about the addressable market.

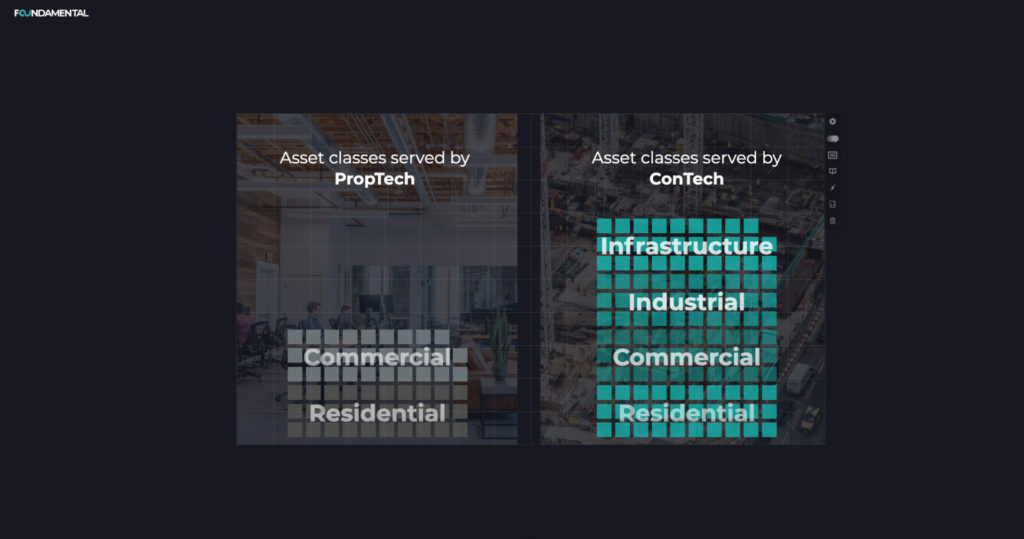

Almost all PropTech addresses two asset classes: residential and commercial buildings.

ConTech is applicable to a larger scope of asset classes. While a large share of companies we see (and like) attack the residential class, and many go after the commercial class, we also see various ConTech firms applicable to infrastructure assets, and some to industrial assets.

Some technologies in construction are vertical and asset-specific. An example of this is auto-generative design, where firms such as PillarPlus auto-optimize MEP for residential assets, other firms such as Continuum Industries auto-optimize waylaying and routing for infrastructure assets such as railways.

And there are examples of construction technologies that can be deployed horizontally across all asset classes, eg. reality capturing such as HoloBuilder.

That being said, most technologies we see (and like) are asset-specific and have a clear vertical focus.

So what’s the point of having more asset classes to serve, if most ventures are vertical and asset-class specific? The point is that the larger market that construction addresses is an advantage for investors.

First, because many of the learnings are transferrable from venture to venture across asset classes.

For example, we learnt from ventures in the high-rise segment that licenses and subscriptions are not well liked by many construction customers, due to project budgeting. This learning actually transfers into the infrastructure and residential segments as well. For us, being an investor in ConTech, seeing what happens in all construction asset classes is a huge advantage to identify patterns across asset classes.

This asset class diversification provides resilience to our portfolio, through optionality and adaptability. A great example we learnt from one of our Asian portfolio firms: Before COVID, the luxury condo build-to-sell space in several Asian economies was booming. The way it worked until COVID was that developers would build high-income condos “on inventory” as there was enough demand pipeline to sell them off at any time during the development. A decent share of our portfolio firm’s revenues came from these high-price development projects.

Since COVID, the infrastructure segment as well as lower-income housing segment are still booming – while the luxury condo segment in that market has yet to rebound. This has stretched the balance sheet – and more so, cash flows – of high-income condo developers, as they sit on inventory against a disrupted market demand in these Asian economies. The average Days Sales Outstanding (DSO) in this asset class increased from 50 days pre-COVID to 120+ days since COVID.

As a reaction, our portfolio firm stopped serving high-income developers since then, and focuses on the other asset classes – infrastructure and lower-income residential. Result: Our firm is at 700% revenue compared to February 2020 with an average DSO of 50 days and less.

We obviously use this learning to use our options in construction tech, picking firms that serve high growth asset classes.

The point: Construction with its various asset classes allows ventures – and venture investors – for optionality and adaptability. As a result, ConTech portfolios are more resilient and less dependent on market disruptions (such as commercial office buildings or commercial retail assets coming under pressure since COVID).

For us, being an investor in ConTech, seeing what happens in all construction asset classes is a huge advantage to identify patterns across asset classes.

Secondly, PropTech is often seen as a very large addressable market – for good reasons. The global market size of professionally-invested global real estate eclipsed $9 trillion in 2019. Mind you, this is the value of the assets though – not the value of servicing the assets. Except for brokerage solution, almost all PropTech is about servicing the asset. Therefore, in reality, the addressable market size for most PropTech is smaller. Let’s assume 20% of the value of a real estate asset goes into yearly maintenance – that gives a real estate servicing market size of $2 trillion. Still a huge market, of course. (We‘ll admit, this does not account for those assets that had not been transacted in 2019 🤓😊)

Let’s compare: The global construction market size is somewhere between $10 and 12 trillion, and 10% of global GDP. And because almost all of construction value is done as-a-service for the investor of the asset, the total construction market size is practically equal to what can be serviced (i.e. $10-12 trillion annually).

So, the $10 trillion construction market that ConTech companies is even larger than the market that most PropTech’s play in (except for brokerage).

If you are excited about PropTech (rightly so!), you should be even more excited about ConTech (hell yeah!).

For commercial asset investors/owners: Many face a disruptive market shakeup since COVID. By focusing on PropTech, commercial asset owners can optimize top-line and operating cost of a disrupted asset class, be it commercial retail, offices or tourism assets. You have to wonder if this is equal to riding a dead horse – only time will tell, no one can know for sure. But that’s the point, isn’t it? Because owners of commercial assets cannot know if they are riding a dead horse, seeking diversification and new avenues to future growth makes sense. When focusing on ConTech, they gain access to entirely new business.

For residential asset investors/owners: COVID has demonstrated how resilient the residential asset class is in major economies around the globe. The lower-to-mid income residential asset class is thriving. According to the US Census Bureau the number of building permits in April 2021 has increased by 60.9% compared to April 2019. We speak regularly with the CEOs of major asset owners and construction firms – almost uniformly they believe that the lower to mid market residential construction will be a growth driver of economies for the 2020s decade, alongside infrastructure. In the last months, many of them have taken bold strategic decisions to focus more and more on the low-to-mid income residential asset class.

There is a paradox for large residential developers though: While the residential asset class is booming, existing residential portfolios are not on par with economic and climate expectations. Existing portfolios have fallen behind. Large developers that are public or go public might come under shareholder pressure to differentiate more clearly. We observe multiple publicly-listed developers on the verge of upgrading to the highest stock indexes in their countries – which comes with more shareholder scrutiny and questions such as “how do you differentiate from your competitors” and “show me your carbon footprint”. Shareholders are asking for differentiation and new efficiency potentials.

While the servicing of homes has been addressed and optimized for years (PropTech), the design, construction and renovation of residential assets is where we still find massive opportunities to drive throughput and growth (ConTech). Residential asset owners can gain access to a wide range of ConTech opportunities, and thus drive the next level of productivity gains and strategic differentiation.

For infrastructure and industrial asset investors/owners: Existing infrastructure assets can see major ROI from overhauls and life-extension maintenance. That lever is not addressed by PropTechs, but by ConTechs. And then, 1% of GDP goes into building new infrastructure such as highways, tunnels and bridges every year (going all the way up to 5% in China). But almost all of them suffer cost overruns, on average 70% in mature economies. If you are an infrastructure investor with a portfolio of projects, gaining access to ConTech and becoming able to evaluate which technologies are winners, allows you to consider a rollout of the winning technologies across your infrastructure portfolio to reduce cost volatility and increase project transparency and coordination. More cash, less risk across your portfolio.

For building components/materials producers and distributors: In our conversations with the top execs of many of these firms – from New Zealand over Indonesia, Germany, UK to North America – we were impressed how several of them use ConTech as a new customer group. One good example is a global building components manufacturer using venture capital as a sales channel to identify the highest-growth prefab firms across the globe, and get the fast-lane access for sales and partnerships of their products into this high-growth customer segment.

Sales channel for core business: Asset investors/owners use ConTech to gain access to high-growth customers and partners to distribute your core products, i.p. building components and building materials. Examples: bathroom supplies, tiles, windows, insulation, cement/concrete/aggregates, steel and many more.

Productivity gains: You can roll-out ConTech massively over your portfolio of construction projects. Works best if you are the investor/owner and can mandate the application of new technologies, eg. via your tender/RFQ. Examples: reality capturing/digital twin technology, workflow management software, computer vision on site, enhanced wireless networks for sensor integration.

Investor relations: You become able to communicate to shareholders your efforts to strategically differentiate vs. competitors and to reduce your carbon footprint by investing in ConTech and partnering with the very best ConTech firms in your markets. Use the access you gain to stimulate your internal innovation efforts with the impulses you gain from external ConTech.

New business opportunities: This is the longest term game you can play, but also offering the highest rewards. Use your ConTech access to track which of the emerging markets and business segments will be here to stay – what are the growth rates, what are the margins, what playbooks and technologies are winning. This requires deep access “behind the scenes” and is the most difficult to pull off for incumbents on their own. When you succeed, you gain the ability to drive M&A and inorganic growth highly effectively.

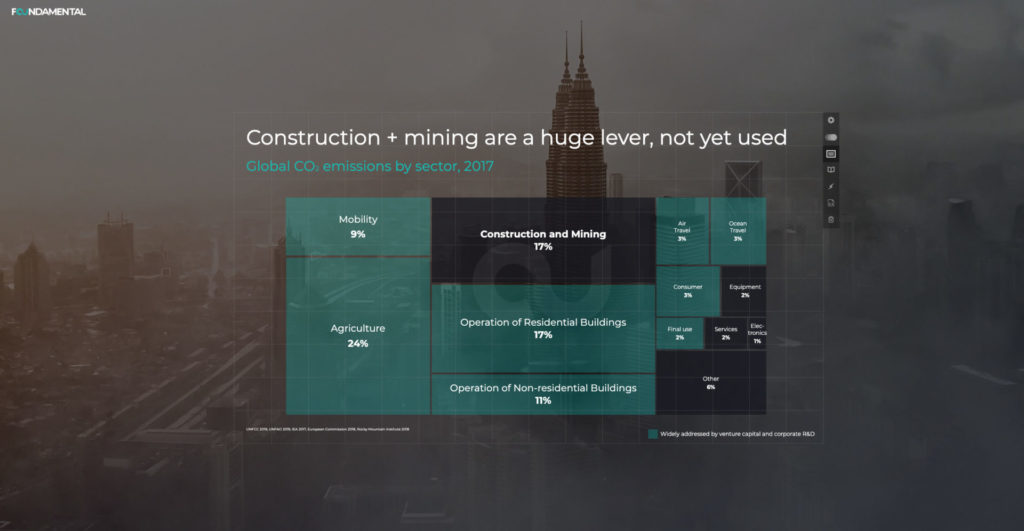

We saved the best for last. Our research and own calculations show that the carbon emissions reduction potential from construction is 10x higher on a per-year per-building basis than when we optimize the existing building stock. Here’s why.

(Before we explain – let’s be crystal-clear: Both new construction and existing buildings will have to massively reduce their carbon footprint to reach the world’s carbon emissions targets. It’s not an OR, it’s an AND.)

Both existing buildings and new construction are big contributors to the world’s carbon emissions (UN, EIA and Rocky Mountain Institute numbers from 2017 and 2018):

What this tells us is that both construction AND existing buildings offer us massive levers to decarbonate the world. And that’s true. But not quite the whole picture.

Consider these numbers for the life time of a prototypical multi-family home:

Now, you might say: “see, the carbon reduction we gain from optimizing building operations are much higher than from construction.”

Over decades, yes. But context helps. Don’t rush to your conclusion just yet. Consider this:

The main difference between construction and existing properties is that construction unfolds over a short time period (say, on average, 2 years construction time) while existing buildings run over long time period (eg. 50 years). Also, existing buildings require major overhauls and renovations (eg. every 25 years).

Now, if you break down the above numbers on a per-year basis, the picture changes:

That is a 10x difference between the emissions from construction vs. the emissions from building operation for the same building.

Also, the construction emissions can be reduced immediately, over the first 1-2 years, while the emissions from building operations unfold over many years.

The point: Construction is the 10x bigger lever to reduce carbon emissions than building operations. ConTech addresses the big instant CO2 lever while PropTech is a lever that unfolds gradually and more slowly.

Finally, consider this. If you master ConTech, you don’t just optimize the construction phase, but the later operations phase as well. By engineering our buildings differently, we also influence the operations during the asset’s whole life cycle. Better insulation during construction means lower operating cost and lower emissions. ConTech has a positive double-effect on both the construction phase and the property management phase.

This doesn’t work the other way round: If you master PropTech, you only optimize the next years of operations, but you won’t optimize construction of your next buildings.

For all of the above reasons, we observe that ConTech is beginning to inflect.

While PropTech has become a massive industry over the past years – and rightly so – we believe ConTech offers exciting growth rates, business opportunities and return potential for asset owners, investors and founders.

We believe that ConTech – alongside HealthTech, FoodTech and a few other sectors – will be THE high-growth sector for the 2020s decade.

Check out my colleague Marie’s article on the data why we think ConTech will inflect 5x-6x in the next 3 years.

And that’s why we feel: ConTech > PropTech in 2021.

Keep in mind: we’re unashamedly biased. We’re just really 🐂 -ish on ConTech.

If you feel like us: We would love to hear from you. 💌